Nvidia Corporation (NASDAQ:NVDA) has been a standout performer over the past year, driven by soaring demand for its AI chips, which has outpaced macroeconomic and geopolitical concerns. Despite Nvidia’s market cap recently climbing by an additional $1 trillion, now exceeding $2 trillion, there are compelling reasons to believe the company’s growth story remains robust, with significant potential for further stock appreciation. I maintain a long position, confident that Nvidia is not yet in bubble territory, despite its aggressive recent growth.

The Rally Continues

Last May, I published an article titled "Nvidia: I Was Wrong," explaining why generative AI is not a passing trend like the metaverse. My conclusion was based on personal experience integrating various generative AI tools into my workflow, significantly boosting my efficiency. In September, I issued my first BUY rating for Nvidia, then trading at around $400 per share, after recognizing that the AI rally was far from over.

In November, I followed up with another article, "Nvidia: The Market Is Wrong," arguing that the market was underestimating Nvidia’s potential, especially the growing demand for its AI chips. Since then, Nvidia’s shares have surged over 80%, adding more than $1 trillion in market cap, with ample evidence that the growth story is still unfolding.

Nvidia’s latest Q4 earnings results, released last month, exceeded expectations, with revenues up 265.3% Y/Y to $22.1 billion, surpassing estimates by $1.55 billion. The Non-GAAP EPS of $5.16 also beat expectations by $0.52.

This exceptional performance underscores that demand for Nvidia’s chips has not peaked, with potential for further earnings beats in upcoming quarters. The ongoing shortages of its flagship AI chips, driven by global demand, and the increasing investment by sovereign nations into AI infrastructure, further bolster Nvidia’s growth outlook.

Nvidia’s dominance in the generative AI chip market faces little threat from competitors. In my latest article on Advanced Micro Devices, Inc. (AMD), I noted that AMD expects to sell only $3.5 billion worth of AI chips in 2024 at lower prices than Nvidia. Nvidia’s recent unveiling of the world’s most powerful AI chip further solidifies its market position.

Given these catalysts, Nvidia’s growth trajectory is set to continue. The company is expected to grow its top line by ~80% in FY25, with similarly aggressive earnings growth.

There’s potential for upward revisions in outlook as the year progresses, which could drive further stock appreciation. Nvidia’s current forward P/E of ~36x is undervalued compared to AMD’s ~50x, and the broad market average of ~28x, indicating Nvidia is not in bubble territory.

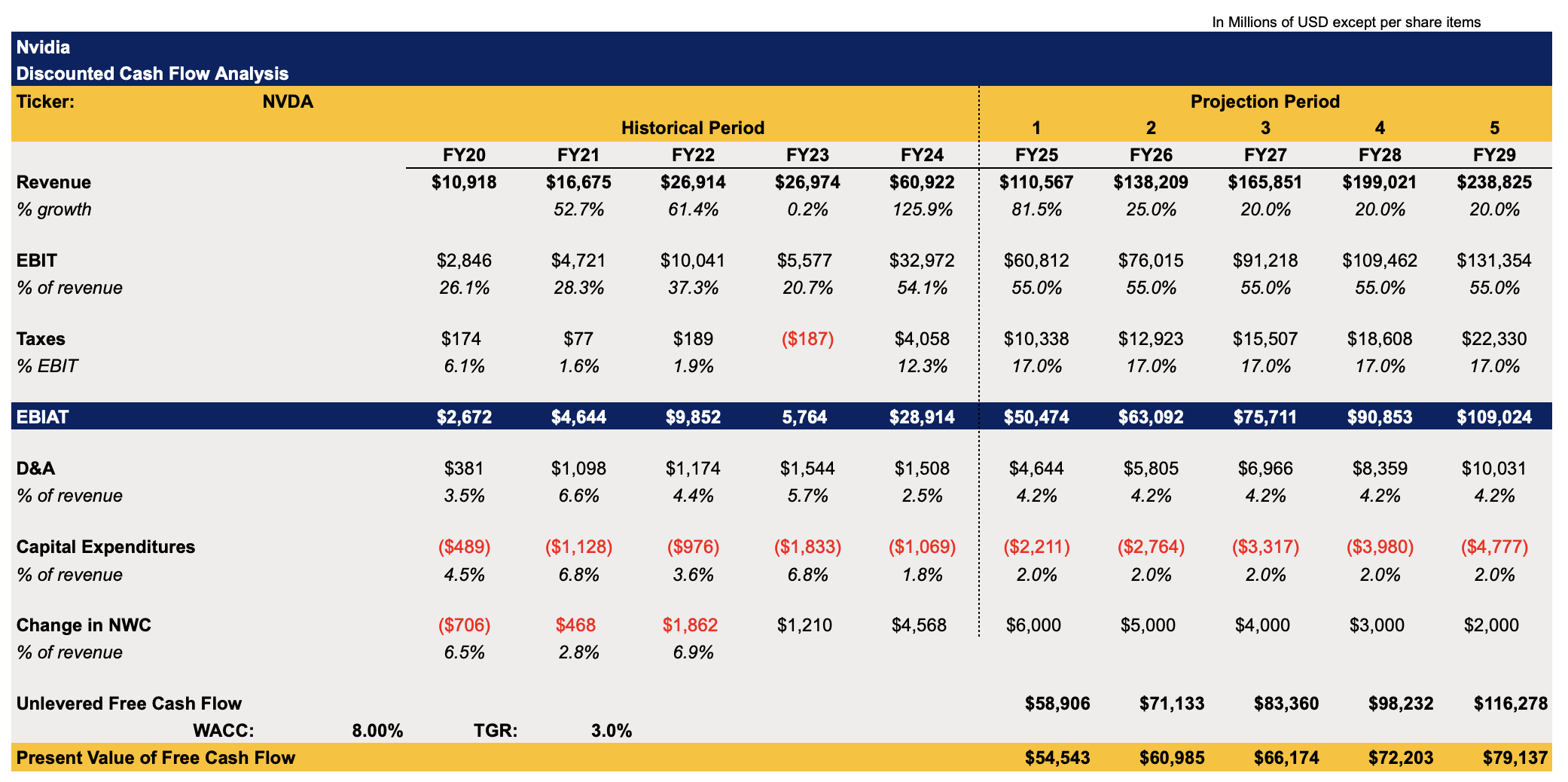

To estimate Nvidia’s fair value, I created a discounted cash flow ("DCF") model, shown below. The revenue and earnings assumptions align with Street expectations, while other metrics reflect historical levels. The model uses an 8% WACC and a 3% terminal growth rate.

Nvidia’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

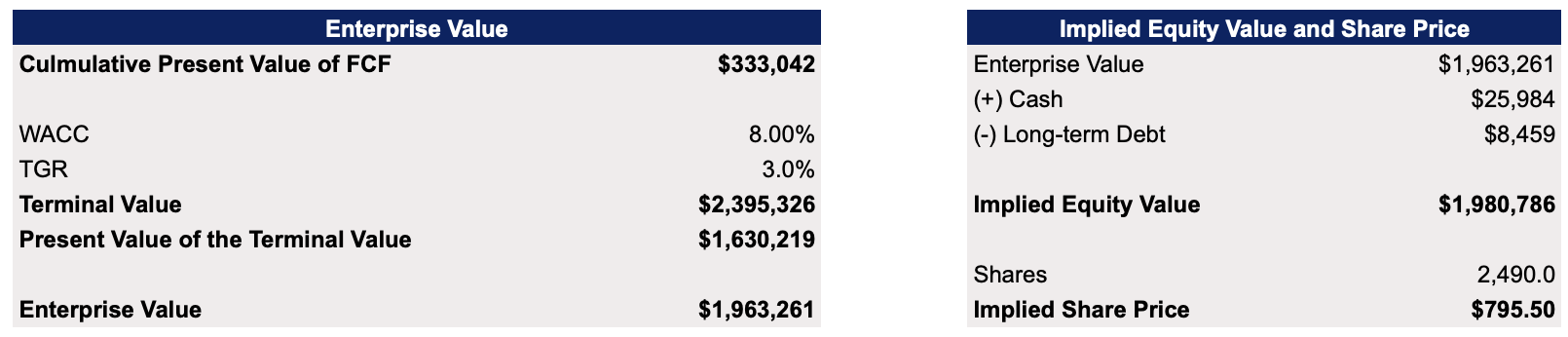

The model indicates Nvidia’s enterprise value is close to $2 trillion, with a fair price of $795.50 per share, below the current market price.

Nvidia’s DCF Model (Historical Data: Seeking Alpha, Assumptions: Author)

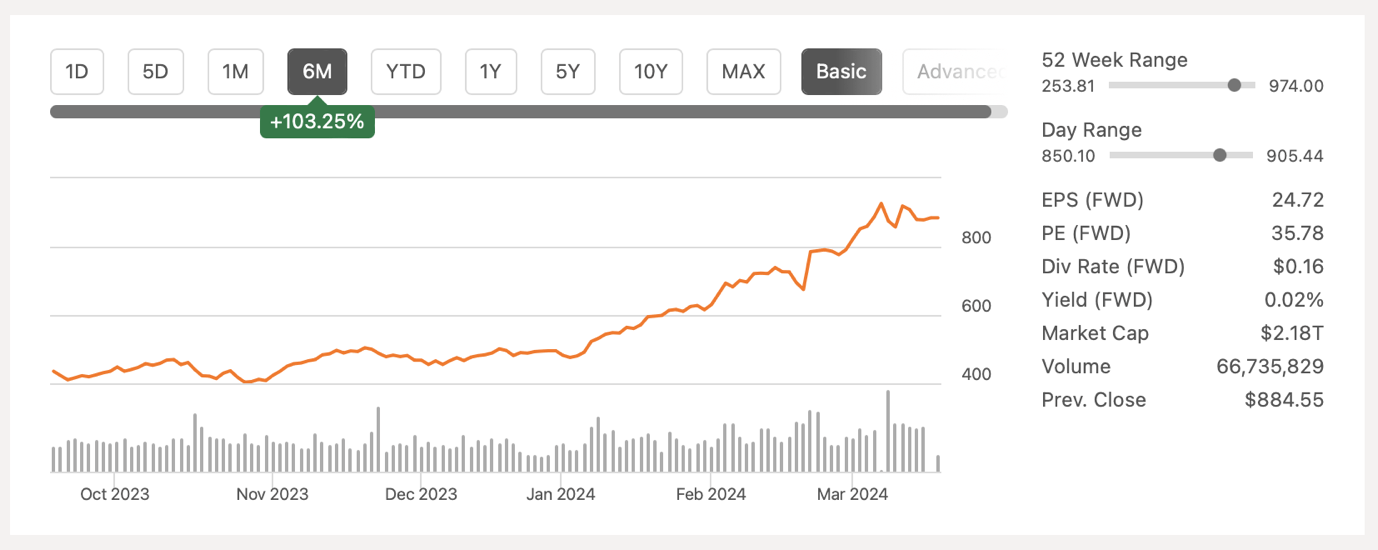

However, the outlook could be raised, prompting upward revisions of the model assumptions, leading to a higher fair value. Nvidia’s shares have found solid technical support above $850, suggesting potential for new all-time highs.

Nvidia’s Stock Price (Seeking Alpha)

Major Risks To Consider

It’s important to acknowledge potential downside risks. Despite current momentum, Nvidia may eventually face challenges exceeding market expectations consistently. When demand peaks, aggressive returns could diminish. Nvidia’s sales in China have declined significantly due to U.S. export restrictions, though this has been offset by demand in other markets. There’s a risk that as demand stabilizes, Nvidia may struggle to find new growth catalysts. However, this scenario may be years away, given current developments.

The Bottom Line

Given the above, I’m holding my long position in Nvidia Corporation stock and maintaining a BUY rating. Nvidia’s growth opportunities currently outweigh major risks. While it may become harder for Nvidia to exceed expectations in the future, it appears we have not yet reached that point.